Capital Allocation

The best way to know if you have a high-quality management team at the helm of a company is to follow the capital allocation strategies. I'd argue, the most important job of the CEO is defining the capital allocation strategy. Especially if the company is public, if you aren't doing your diligence on whether or not the executive team is creating value for you, you shouldn't be stock picking. It's a big deal.

When Meta announced its first dividend in 2024, the stock rose immediately, adding nearly $200 billion in a single day. Although the dividend payout was quite small, 50 cents a share, it was more about the signal the company was sending to the Street.

Since its IPO, Meta had been a Big Tech company that was a so called "growth at any cost" type of stock. The company had spent billions on moonshot projects such as the metaverse. The dividend was a signal to investors that the company was maturing and becoming more thoughtful about creating shareholder value.

Once a company can no longer internally invest money at a rate higher than its cost of capital, it should look to return cash to shareholders. Although I'm not a huge fan of returning cash via dividends, (more on this in a future topic) I prefer stock buybacks. (As long as the company buys back stock when it is at a discount to its intrinsic value.)

Investors have a habit of focusing mostly on product launches or recent earnings, and let's be real, these are a little more exciting topics to cover than capital allocation. However, the best CEOs understand value creation and protect the shareholders of the company.

ROIC and WACC

My apologies for the alphabet soup, but if I could only pick one metric to assess a stock, it would be the difference, or the spread between the Return on Invested Capital (ROIC) and the Weighted Average Cost of Capital (WACC).

Every company raises capital from shareholders or lenders. The cost of raising that capital is the WACC. Companies then invest the money they have raised on various projects or initiatives to generate a return, this is the ROIC.

The results are simple, but critical to the success of a company.

-

ROIC > WACC: Every dollar invested creates value, growth is good for shareholders.

-

ROIC < WACC: Every dollar invested destroys value, growth is bad for shareholders.

I know what you are thinking, this seems pretty obvious, but the market has a way of selling the story of the new and exciting tech stock as a "growth story." These types of companies get a pass because their future growth is expected to more than make up for burning cash. But, these companies will need to raise capital to stay in business, so you will probably be diluted at the next cash raising event. It's why the new growth stocks are so speculative in nature.

Before you buy a stock, check the spread. If the ROIC is lower than the WACC, that company is currently burning cash.

True Profit

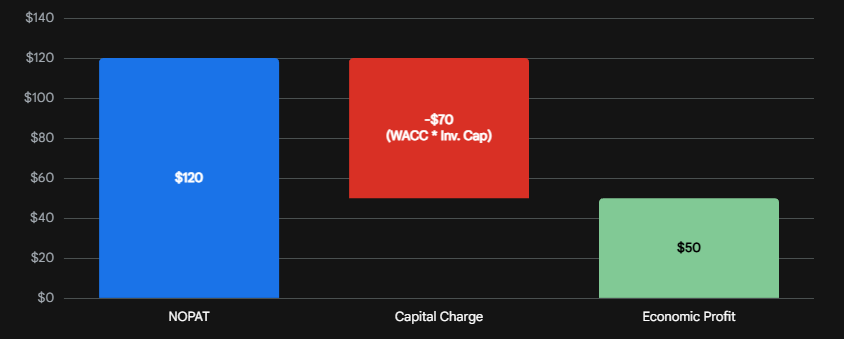

Once you understand money isn't free, you can figure out if a company is truly profitable. The best way to do this is figuring out the Economic Value Added (EVA). This metric factors in the return you, the shareholder, should expect from the company.

A company can have a healthy Operating Profit and still have negative Economic Profit. It's another way to explore if the company is providing shareholders value, or if they are destroying it.

From Accounting Profit to Economic Profit

Economic Profit Waterfall

CEO Decisions

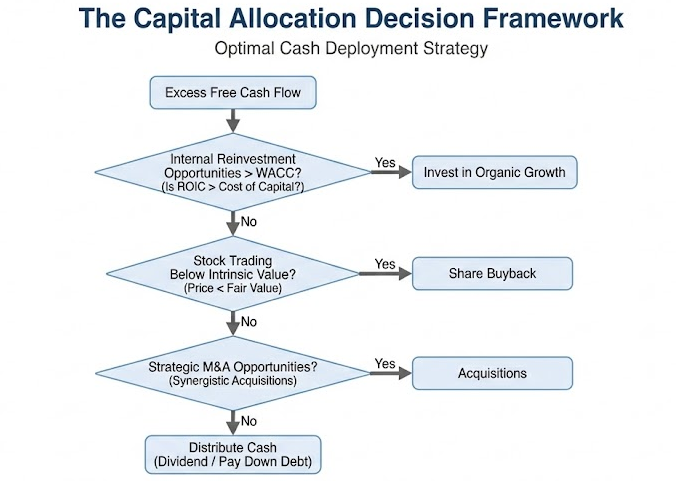

Now that we understand how to assess if a company is creating value. Let's get back to how the CEO thinks about capital allocation.

There are five options for excess cash.

- Invest back into the business

- Acquisitions

- Pay down debt

- Pay dividends

- Buy back stock

If a company can't reinvest its cash at a high rate (ROIC > WACC), it needs to give the money back to you.

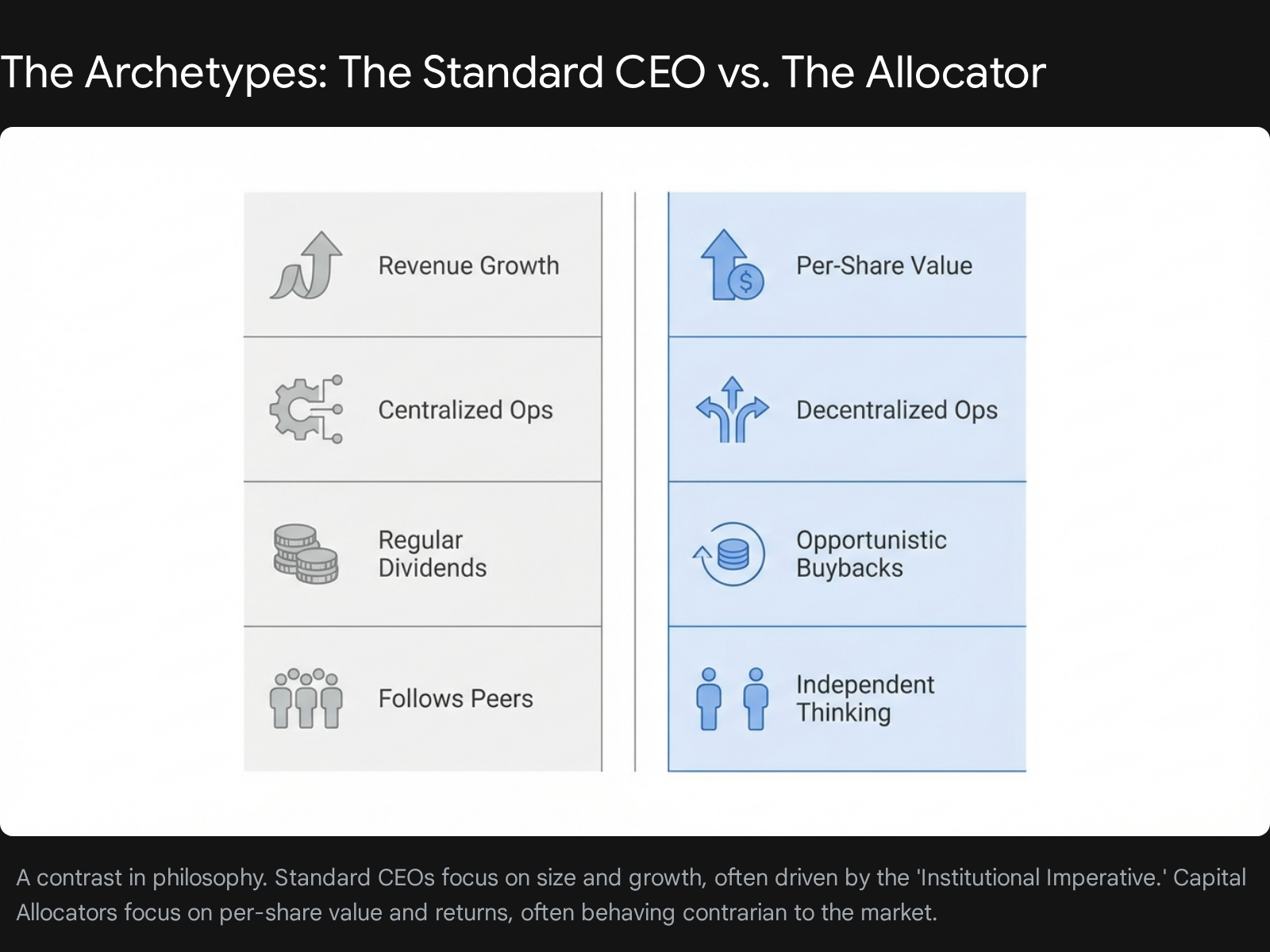

The chart below shows the differences between a standard CEO and a true Capital Allocator. Once you know how to assess the difference, you realize, there are not many CEOs that really manage their capital allocation strategies to benefit you, the shareholder. If you find one that does, best to hold for the long term as they are creating value for you.

In summary, check the spread, economic profit, and buybacks. Look for more on this in future deep dives on the website.

Latest News

The Mid-Cap Bellwethers ($2B – $10B)

- Beat. EPS of $0.62 (vs. $0.59 est) | Revenue $690.6M.

- While revenue missed estimates (coming in at $690.6M vs. the $699M expected), the bottom line beat is key. Credit quality and efficiency are winning over investors nervous about regional banking volatility.

Knight-Swift Transportation (KNX)

- Miss. EPS of $0.31 (vs. $0.36 est) | Revenue $1.86B.

- The freight recession drags on. Knight-Swift missed estimates as pricing power remains elusive; management signaled that while the "destocking" phase is over, the shipping volume recovery is flatter than the market priced in for early 2026.

- Strong Beat. EPS of $0.94 (vs. $0.79 est) | Revenue $465M.

- The specialty insurer continues to be a cash machine by dodging broader industry margin compression. RLI’s focus on niche markets (like surety and property coverage) allows it to outperform generic auto/home insurers.

The Small-Cap Signals (<$5B)

Winmark Corporation (WINA)

- S&P Dow Jones announced Winmark will join the S&P SmallCap 600 next week (replacing Guess?, Inc.).

- The stock popped ~5% as index funds began their mandatory buying, marking the franchisor's graduation to the major leagues.

- Beat. EPS of $1.55 (vs. $1.46 est).

- This Walla Walla-based bank serves as a proxy for the Pacific Northwest, and results signal regional strength. Loan growth held up better than expected, suggesting businesses in Washington and Oregon are still borrowing despite the rate environment.

- Despite solid operational progress, the nerve-repair biotech announced a $124 million public offering to pay down debt and fund growth.

- Shareholders rarely like dilution; the stock is trading down sharply in the pre-market as the market digests the new supply of shares.

Movers and Shakers

- Teledyne (TDY): Up 6.5%. The defense and sensor tech firm rose after strong earnings, proving that high-tech defense spending remains "sticky" in a tense geopolitical world.

- Axogen (AXGN): Down 7%. The secondary offering mentioned above is acting as a lead weight on the stock this morning.

- Winmark (WINA): Up 4.6%. The "index effect" is in full swing, driving volume and price higher before the bell.

The Briefing

- Jobless Claims (8:30 AM ET): The market is looking for confirmation that the labor market is cooling gently rather than stalling out.

- Leading Economic Indicators (LEI): Later this morning, these data points will clarify if recession risks for late 2026 are fading or growing.

Today's Fun

The Ticker Test

Since we covered index changes today (Winmark joining the S&P 600), let's test your knowledge of creative stock tickers.

Question: Many companies choose ticker symbols that double as marketing. Which of the following mid-cap companies trades under the ticker symbol "EAT"?

A) Domino's Pizza

B) Brinker International (Chili's/Maggiano's)

C) The Cheesecake Factory

D) US Foods

(Scroll down for the answer)

Thank you for spending part of your morning with me. See you tomorrow. -Marques

Sign up here to get this newsletter in your inbox. Reach our team at marques@blankcapitalresearch.com

Answer: B) Brinker International.

The parent company of Chili's and Maggiano's Little Italy trades as EAT.

(Bonus fact: The Cheesecake Factory trades as CAKE, and Ferrari trades as RACE.)