| ↑ End of paid message | The Capital Memo |

|

Catarina Custódio published Mergers and Acquisitions Accounting and the Diversification Discount in the Journal of Finance in 2014. Her finding cut deeper. When a company makes an acquisition, the accounting writes up the target's assets to fair market value at closing. That write-up systematically inflates the book value of the diversified firm relative to its standalone-firm comparables. The diversified firm looks artificially expensive on certain book-based multiples and artificially cheap on the comparable-firm benchmarks the discount studies relied on. Custódio showed that controlling for this accounting effect, the discount shrinks meaningfully for the M&A-active subset of conglomerates, which is most of them. The original finding from 1995 was real, but a substantial portion of the magnitude was a measurement artifact rather than economic value destruction. |

| | The textbook claim, by 2015, looked like this. Conglomerates destroy value some of the time, in conditions the literature can specify. Outside those conditions, the case is much weaker than the 1990s findings suggested. Berkshire fits squarely outside. |

|

Why steady compounders trade cheap. |

Todd Mitton and Keith Vorkink published the third paper in the Journal of Financial and Quantitative Analysis in 2010. Their question reframed the discount entirely. If the discount exists, why? And what does it predict for future returns? Their answer drew on a different strand of asset pricing. Investors prefer assets with positive skewness. Lottery tickets. Concentrated single-business firms with the chance of explosive upside. Diversified firms, almost by definition, smooth out their return distributions. Five segments offsetting one another rarely produce a ten-bagger. The chance of an extreme positive outcome is structurally lower in a five-segment conglomerate than in a single-product growth company. Investors who care about skewness, disproportionately retail, momentum-chasing, and short-horizon, bid up single-business firms and discount diversified ones. The discount is real. It is also compensation for less lottery-style upside. Mitton and Vorkink showed that diversified firms therefore earn higher expected returns going forward, on average, precisely because they offer lower realized skewness. The discount becomes the source of the return, for an investor who does not need lottery upside. Most readers of this newsletter are exactly that kind of investor. |

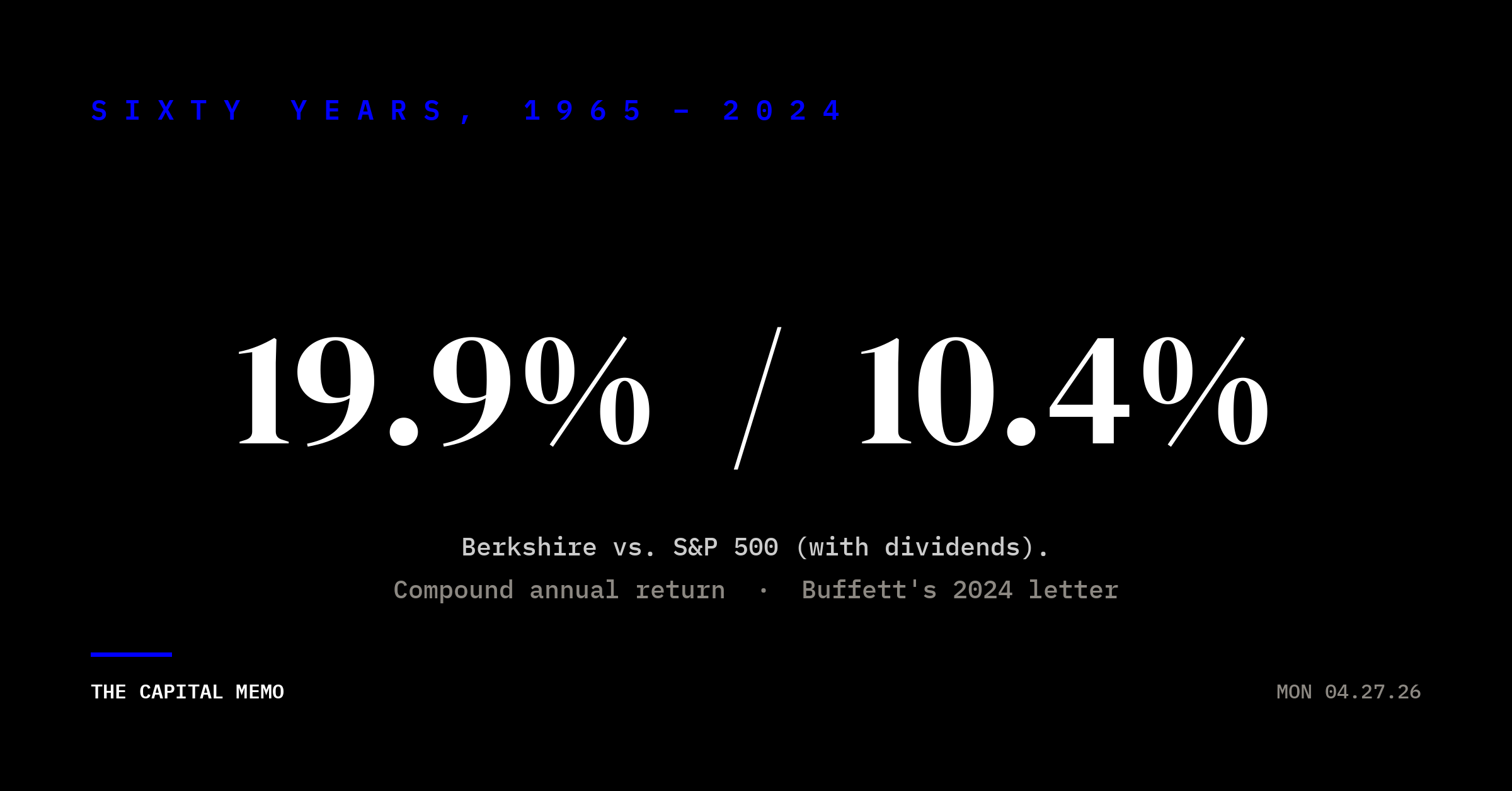

| Sixty years, 1965 – 2024 19.9% / 10.4% Berkshire compound annual market value vs. S&P 500 with dividends. Buffett's 2024 letter. |

What Abel has to demonstrate. |

Read together, the three papers complicate the simple version of the discount story. The discount is conditional on internal capital allocation discipline. Some of the apparent magnitude is a measurement artifact. And whatever discount remains is structurally compensation for lower lottery-style upside, which on average means higher expected returns going forward. Berkshire's sixty-year track record fits this revised picture. Internal allocation has been disciplined. The return profile has been steady rather than lottery-like. Each of those features traces to specific institutional choices. The market's question for Saturday is whether those choices survive Abel's tenure. The fourteen-percent decline in Berkshire shares since the retirement announcement is the market's preliminary vote that the alpha left with Buffett. The academic literature suggests that vote is premature. Some of the discipline that produced sixty years of nineteen-and-a-half-percent compounding was Buffett personally, and that part is gone. Much of it was institutional. Internal capital allocation rules. Decentralized operations. Insurance float as a low-cost funding source. Concentrated decision-making at headquarters with operational autonomy at the subsidiaries. The institutional features can survive a CEO change. Whether they do is what Saturday tests. What Abel needs to demonstrate Saturday is continuity in the institutional rules that produced the academic profile in the first place. Three things specifically. The cash deployment plan. Berkshire ended Q3 2025 with about $381 billion in cash and Treasuries. That is the largest cash position in corporate history. Buffett's framework for deploying it has been discipline plus patience. Abel needs to show shareholders that the rules are unchanged, even if the deployer is. The buyback signal. Berkshire resumed share repurchases in March, the first time since 2024. UBS estimates the stock is trading at roughly an eight-percent discount to intrinsic value. Henry Singleton at Teledyne, the canonical Outsider profile, would have been a heavy buyer at that level. Abel's pace from here will tell shareholders whether he reads valuation the same way Buffett did. The technology question. Berkshire's historical underweight in technology was a deliberate choice rooted in Buffett's stated discomfort with predicting return on capital in fast-changing industries. The market wants to know whether Abel will run the same circle of competence or expand it. The right answer, by the academic framework, is whatever preserves the discipline of investing only where return on incremental invested capital is calculable with confidence. Whether that includes more technology than it used to is a question of judgment, not philosophy. |

| → The takeaway The financial press will spend the week framing Saturday as the post-Buffett era. That framing is true, and it is also incomplete. The deeper question is whether the academic profile of Berkshire as a structurally well-built conglomerate, rather than as Buffett's personal vehicle, holds up under a new operator. Three papers from the last twenty-five years already specified what to look for. Saturday gives us live data. Have a good Monday. — Marques |

| About the author Marques Blank is the founder of Blank Capital Partners and Blank Capital, a fractional CFO and FP&A advisory. Former Northrop Grumman ($1.6B business unit) and Citibank (securitized credit). CMA, MBA, Series 65. Sources Berger, P.G., & Ofek, E. (1995). Diversification's effect on firm value. Journal of Financial Economics, 37(1). · Lamont, O. (1997). Cash flow and investment: Evidence from internal capital markets. Journal of Finance, 52(1). · Rajan, R.G., Servaes, H., & Zingales, L. (2000). The cost of diversity: The diversification discount and inefficient investment. Journal of Finance, 55(1). · Mitton, T., & Vorkink, K. (2010). Why do firms with diversification discounts have higher expected returns? Journal of Financial and Quantitative Analysis, 45(6). · Custódio, C. (2014). Mergers and acquisitions accounting and the diversification discount. Journal of Finance, 69(1). · Berkshire Hathaway 2024 annual letter and 2026 proxy statement. Q3 2025 cash position from Berkshire 10-Q. For informational purposes only. Not investment advice. Specific securities mentioned are case studies, not recommendations. Stock performance figures are approximate and based on publicly reported sources as of publication. |

|