Abstract

The Technology Software Application sector represents a distinct asset class characterized by high intangible capital intensity, increasing returns to scale, and network-driven market structures. This paper synthesizes three decades of peer-reviewed financial and economic literature to construct a rigorous investment framework for the sector.

We examine the structural shift from tangible to intangible capital, the systematic failure of Generally Accepted Accounting Principles (GAAP) to capture software value, and the superior predictive power of alternative metrics such as R&D intensity, Customer-Based Corporate Valuation (CBCV), and Implied Equity Duration.

The evidence suggests that traditional earnings-based valuation models are ill-suited for this sector, and that excess returns (alpha) are most reliably predicted by unit-economic efficiency and information asymmetry indicators.

1. Introduction: The Shift to the Intangible Economy

The fundamental investment thesis of the software sector is rooted in a structural transformation of the production function. Unlike the industrial economy, where value creation was driven by tangible assets (Property, Plant, and Equipment), the software economy derives value almost exclusively from intangible assets: proprietary code, organizational capital, and network structures.

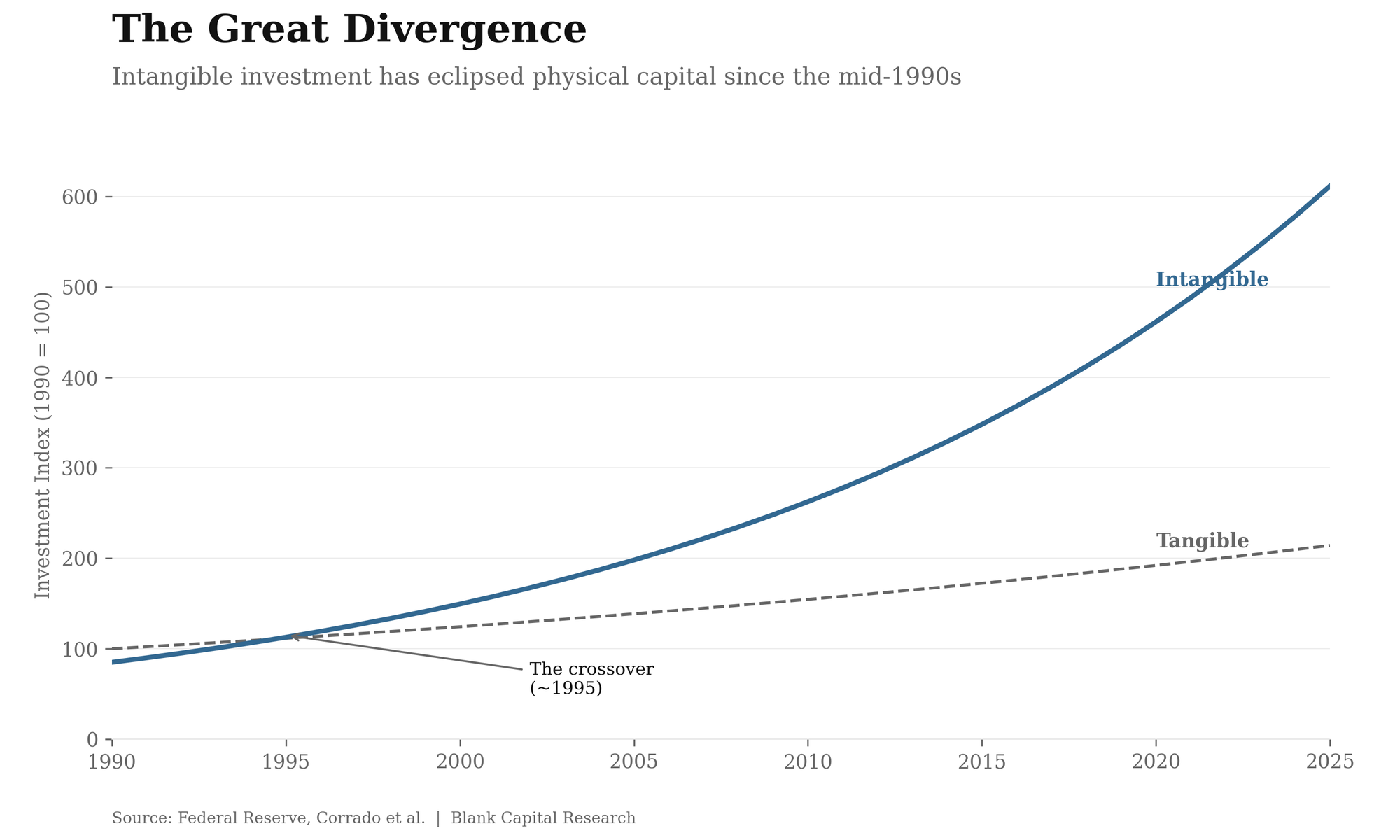

Research by Corrado, Hulten, and Sichel (2009) estimates that investment in intangible assets has exceeded investment in tangible assets in the US economy since the mid-1990s. For the investor, this means we have to dig a little deeper on our analysis. Standard accounting frameworks (GAAP/IFRS) were designed for the industrial age. As noted by Lev and Gu (2016), the "relevance of financial reporting" to stock prices has declined significantly over the past half-century.

This deterioration is most pronounced in the software sector, where the immediate expensing of Research and Development (R&D) and customer acquisition costs, investments that generate future economic benefits, systematically depresses reported earnings and book values.

Successful investment in the software sector requires a departure from "factory-era" metrics (P/E, Price-to-Book) in favor of an evidence-based approach that accounts for the unique microeconomics of digital goods.

2. Structural Economics

To understand the sector's return potential, one must analyze the cost structures and competitive dynamics that differentiate software from physical goods.

2.1 Supply-Side Economics: Zero Marginal Costs

In his foundational work on Endogenous Growth Theory, Paul Romer (1990) distinguishes between "rival" and "non-rival" goods. A physical machine is a rival good; it can only be used by one worker at a time. Software code is non-rival; it can be used simultaneously by millions without depletion.

Shapiro and Varian (1998) describe this as "supply-side economies of scale." Software production is characterized by high fixed costs (writing the code) but near-zero marginal costs (reproduction and distribution). In traditional manufacturing, returns to scale eventually diminish due to capacity constraints and rising input costs. In software, returns to scale are theoretically infinite.

This cost structure creates massive operating leverage. Once a software firm covers its fixed R&D costs, incremental revenue flows almost entirely to the bottom line. Empirical evidence suggests that investors should prioritize Gross Margin as a leading indicator of long-term profitability potential. High gross margins (>70%) indicate that the firm has successfully overcome the initial fixed-cost hurdle and is positioned for profit expansion.

2.2 Network Effects

While supply-side economies drive margins, demand-side economies drive market power. Network Effects are defined as the condition where the utility of a product increases with the number of other agents consuming it.

- Direct Network Effects: Common in communication software (e.g., Slack, Zoom), where the product becomes intrinsically more valuable as more users join.

- Indirect (Two-Sided) Network Effects: Analyzed by Rochet and Tirole (2003), this occurs in platforms (e.g., App Stores, Operating Systems). A growing user base attracts third-party developers, whose applications increase the platform's value, attracting further users.

Gallaugher and Wang (2002) provided empirical evidence in the web server market showing a significant positive correlation between market share and pricing power. Their findings support the "Winner-Take-All" thesis: the leading software firm in a vertical often captures a disproportionate share of economic rent, justifying a significant valuation premium over competitors.

2.3 Switching Costs and Lock-In

The durability of software cash flows is protected by switching costs. Chen and Hitt (2002) studied the determinants of customer retention in internet-enabled businesses. They found that system integration creates high "procedural switching costs."

In B2B Enterprise Software (SaaS), switching vendors requires data migration, staff retraining, and workflow re-engineering. This "lock-in" reduces the price elasticity of demand, allowing mature software firms to raise prices annually without triggering churn, a critical inflation-hedging characteristic for equity portfolios.

3. The Valuation Disconnect: Accounting vs. Reality

A central theme in academic finance is the market's inefficiency in pricing software innovation due to accounting distortions.

3.1 The R&D Anomaly

Under US GAAP, internally generated R&D is treated as an operating expense. However, Lev and Sougiannis (1996) demonstrated that R&D spending behaves like a capital investment. It generates future economic benefits that persist for years. By expensing R&D immediately, high-growth software companies artificially depress their current reported earnings.

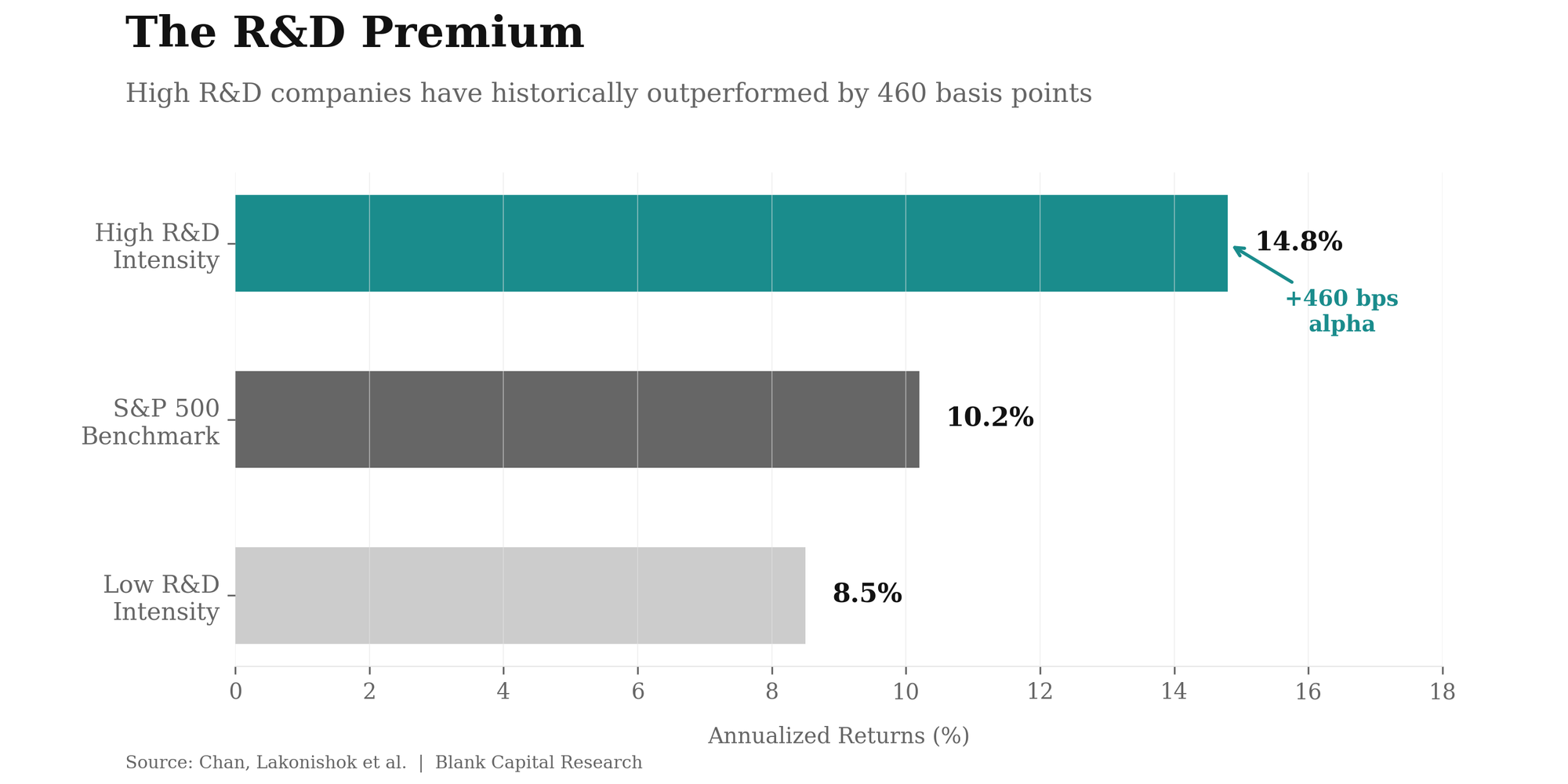

Another study by Chan, Lakonishok, and Sougiannis (2001) in The Journal of Finance investigated the relationship between R&D spending and stock returns. They found that firms with high R&D intensity (R&D expenditures relative to sales) significantly outperformed the broader market over long horizons.

- Mechanism: The market suffers from "functional fixation," penalizing firms for low reported earnings while failing to capitalize the value of the R&D asset.

- Strategy: Investors can generate alpha by manually "capitalizing" R&D expenses (amortizing them over 3-5 years) to calculate an "Adjusted Earnings Multiple." This often reveals that optically expensive software stocks are fundamentally undervalued relative to their true economic earnings.

3.2 Information Asymmetry and Insider Trading

The opacity of software development creates a unique risk/reward profile. Aboody and Lev (2000) found that R&D-intensive firms exhibit significantly higher "information asymmetry" than firms with tangible assets. Because the progress of code development is invisible to outsiders (unlike a factory floor), insiders possess a substantial informational advantage.

- Finding: Insiders in software firms realize consistently higher abnormal returns from their trades than insiders in other sectors.

- Implication: For external investors, monitoring insider transaction data (Form 4 filings) is a more critical signal of future performance in the software sector than in any other industry.

4. Valuation Frameworks: The SaaS Paradigm

The transition to Software-as-a-Service (SaaS) has shifted the unit of analysis from the firm level to the customer level.

4.1 Customer-Based Corporate Valuation (CBCV)

Gupta and Lehmann (2003) pioneered the framework of viewing a firm as a portfolio of customers. In the subscription economy, the value of the firm is the aggregate Net Present Value (NPV) of current and future customer relationships.

McCarthy and Fader (2018)formalized this into "Customer-Based Corporate Valuation" (CBCV) for publicly traded firms. Their empirical work demonstrates that bottom-up models based on customer retention and acquisition often outperform top-down analyst consensus.

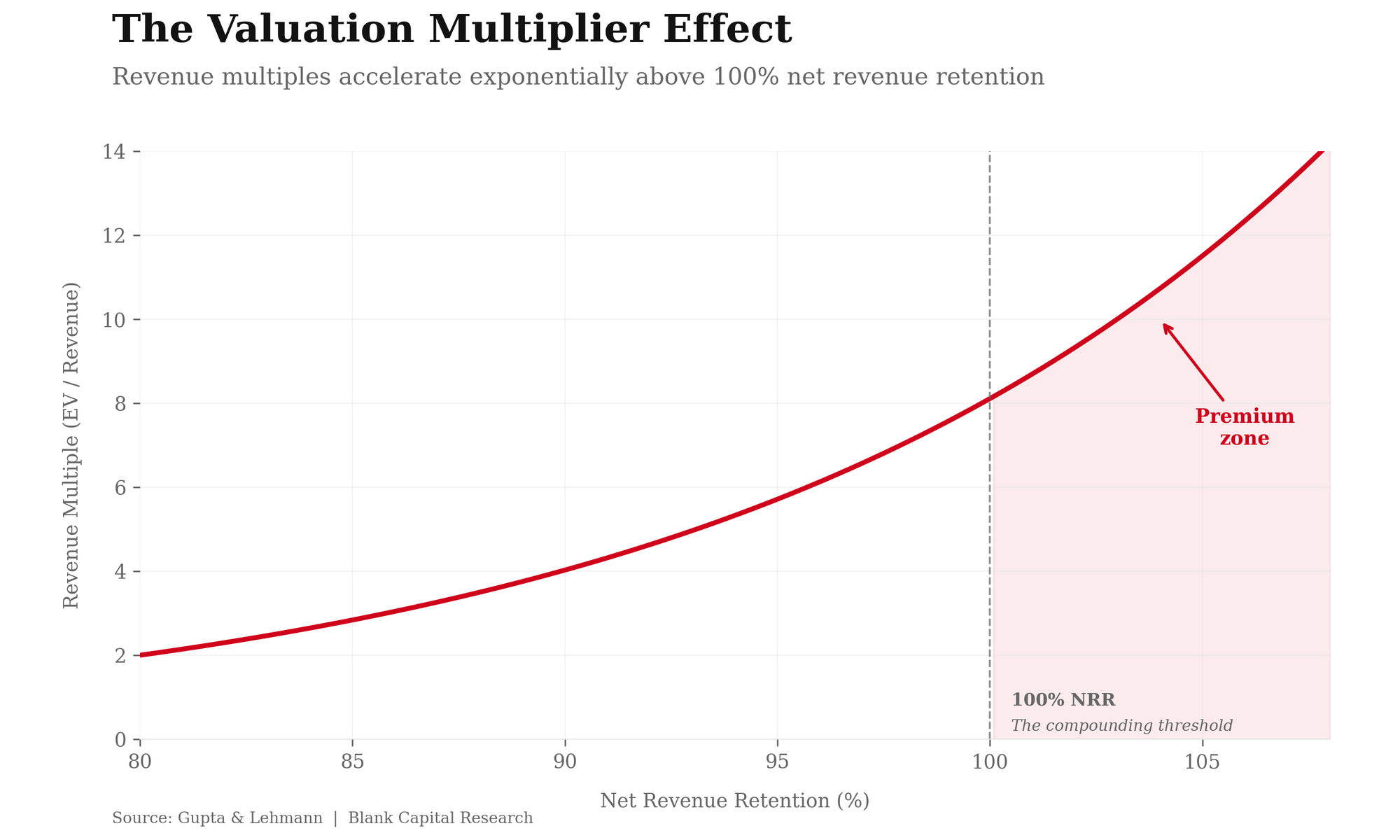

- Key Insight: The model highlights the non-linear sensitivity of Retention.Gupta et al. (2004)showed that a 1% improvement in retention has a significantly larger impact on firm value than a 1% reduction in discount rate or acquisition costs. This validates the investment focus on "Net Revenue Retention" (NRR) as the primary indicator of software quality.

4.2 Real Options Valuation

Traditional Discounted Cash Flow (DCF) models often punish software stocks for their high volatility (via a higher Beta/Discount Rate). However,Schwartz and Moon (2000)applied Real Options Theory to internet and software valuations. They argue that high volatility increases the value of the "growth option"—the ability of the firm to pivot its code to new, unforeseen market opportunities.

Implication: In this framework, volatility is not merely risk; it is potential. This explains why software firms often trade at multiples that imply growth rates higher than their current trajectory; the price includes the "option premium" of future innovation.

5. Risk Profile: Duration and Macro-Sensitivity

While the sector offers high return potential, it is uniquely sensitive to the cost of capital.

5.1 Implied Equity Duration

Dechow, Sloan, and Soliman (2004) introduced the concept of "Implied Equity Duration" to the stock market. Just as long-term bonds are more sensitive to interest rate changes than short-term bonds, "long-duration" equities are highly sensitive to the discount rate.

- Analysis: Software companies are the quintessential long-duration asset. They often have low (or negative) current cash flows but high expected future cash flows.

- Evidence: Dechow et al. (2021) analyzed market behavior during the COVID-19 pandemic and subsequent recovery. They found that high-growth software stocks acted as long-duration instruments, rallying aggressively when rates fell and correcting sharply when rates rose.

- Strategy: Investors must recognize that a portfolio of software stocks carries a massive implicit "short rate" position. Valuation multiples in this sector will expand and contract based on the 10-year Treasury yield, often independent of underlying operational performance.

5.2 The "Rational Bubble" Hypothesis

Pástor and Veronesi (2009) addressed the boom-bust cycles common in tech. Their model suggests that high valuations and high volatility during the adoption of new technologies (like AI or Cloud) are not irrational "bubbles" but a rational response to uncertainty. When a technology's potential is massive but its winner is uncertain, rational pricing dictates high valuations for the sector as a whole. As the market matures and uncertainty resolves, valuations naturally compress.

6. Conclusion and Key Takeaways

The academic evidence indicates that the Technology Software Application sector offers structural advantages, specifically zero marginal costs and network effects, that can drive alpha over long horizons. However, capturing these returns requires a specialized analytical toolkit.

Key Evidence-Based Takeaways:

- Adjust the Accounting: Capitalize R&D expenses to see the true earnings power (Chan et al., 2001).

- Focus on Retention: In SaaS, NRR and the CLV/CAC ratio are the most potent predictors of value (Gupta & Lehmann, 2003).

- Respect the Macro: Understand that software is a long-duration asset; interest rate shifts will drive valuation multiples more than short-term earnings beats (Dechow et al., 2004).

- Value the Moat: Invest in firms with demonstrable network effects and switching costs to ensure the durability of cash flows.